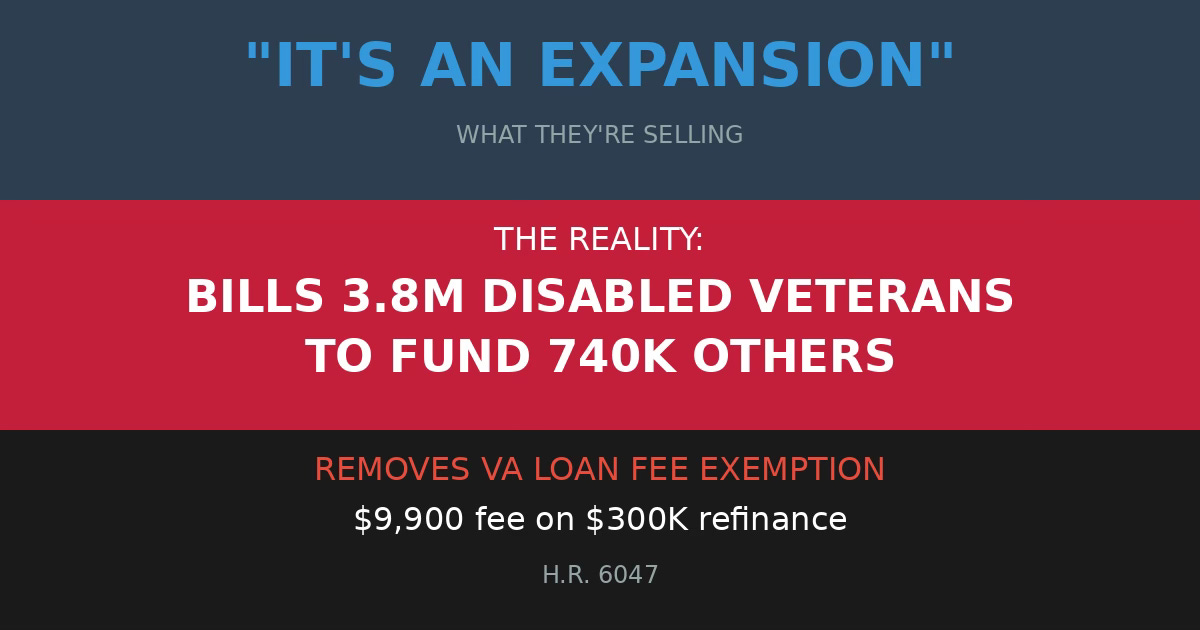

F#@k You for Your Service: H.R. 6047 and the Veterans Congress Robs to Pay Other VeteransThey named it after real veterans. They'll fund it by charging disabled veterans thousands in fees they don't pay now. And they'll call it an expansion.Tbird's Quiet FightDec 05, 2025∙ Paid21ShareContinue reading this post for free, courtesy of Tbird's Quiet Fight.Claim my free postOr purchase a paid subscription.PreviousNext